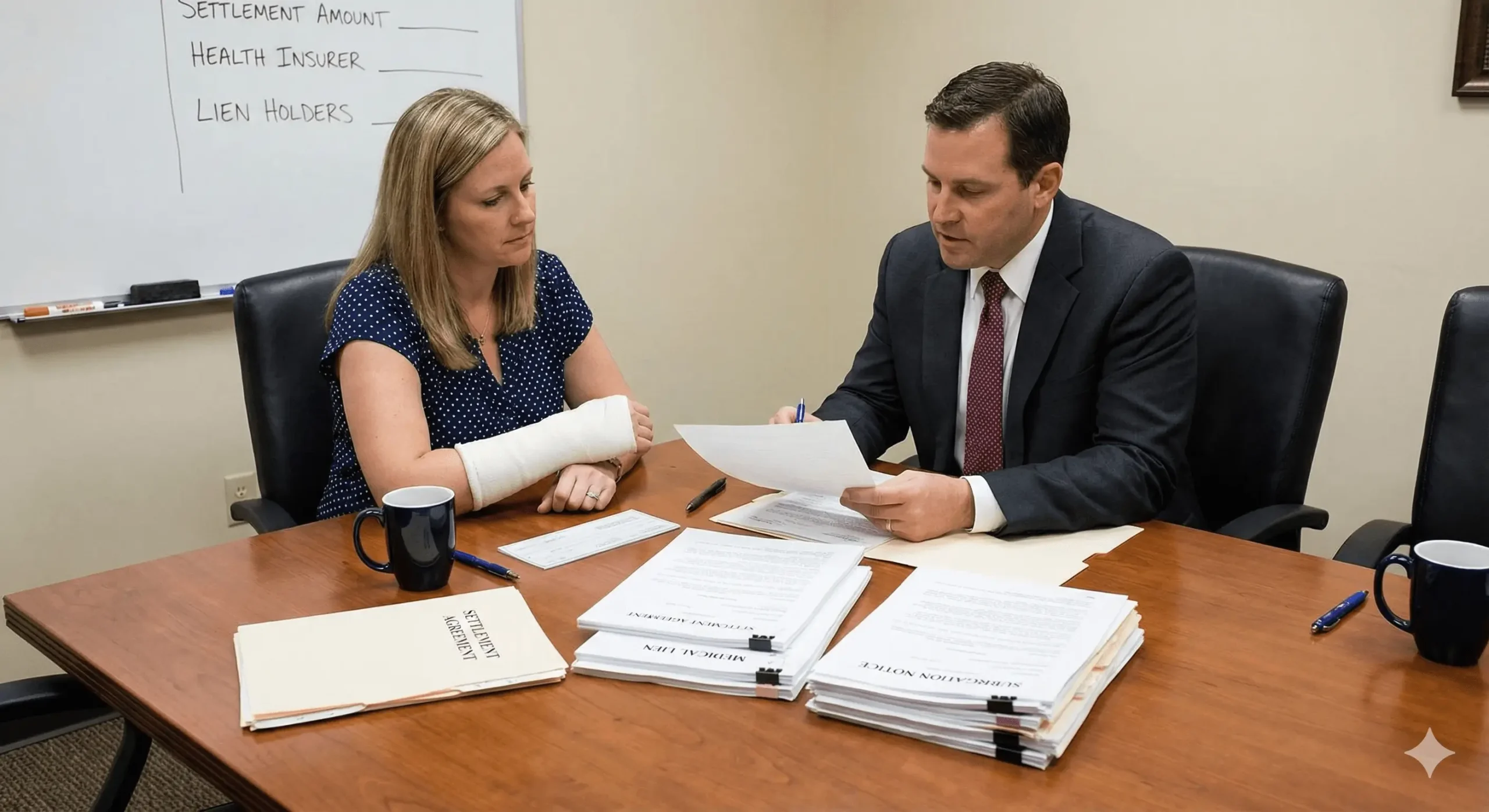

Medical Liens & Subrogation: Who Gets Paid First After an Injury Settlement?

In most personal injury cases, the injured party is typically last to receive money from a settlement. Before any funds are released, attorney fees and case costs, federal reimbursement claims, insurance subrogation demands, and valid medical liens must be identified, verified, negotiated where appropriate, and paid.

This priority system explains why a settlement can look substantial on paper but result in a much smaller net payout once legally enforceable claims are resolved. If your injury case is in Florida or Texas, certain lien and recovery rules can affect negotiation leverage and how specific claims are handled.

Who Gets Paid First After an Injury Settlement?

This question comes down to legal priority multiple parties may have enforceable rights against the same settlement funds.

The Settlement Payment Hierarchy Explained

In many injury cases, settlement proceeds are distributed in a priority order that often includes:

- Attorney fees and case costs

Compensation for legal representation plus expenses required to obtain the recovery. - Federal reimbursement claims

Commonly Medicare or Medicaid, which may hold priority repayment rights. - Child support arrears

When applicable, past-due child support may be deducted under governing law. - Private health insurance subrogation

Reimbursement demands for accident-related care paid by health insurance. - Medical provider liens or Letters of Protection

Claims asserted by hospitals or treatment facilities tied directly to settlement funds. - The injured party

Any remaining balance, commonly called the net settlement.

This structure frequently appears in serious injury matters, including those described in common types of personal injury cases:

Why a $100,000 Settlement Can Become a Much Smaller Net Payout

The reduction is rarely about “missing money.” It reflects how settlement funds are allocated to repay treatment costs and resolve legally enforceable claims.

A Practical Example

Using simplified numbers for illustration only:

- Attorney fees and costs are deducted first

- Federal reimbursement claims may follow

- Insurance subrogation and medical provider liens are then addressed

Two cases can settle for the same amount and produce very different net results depending on lien size, validity, priority, and negotiability.

What Is Medical Subrogation and Why Does It Reduce Your Settlement?

Subrogation allows an insurer to seek reimbursement when it paid for accident-related care and a third party later pays damages through a settlement.

How Health Insurance Subrogation Works

When health insurance pays for emergency treatment, surgery, or rehabilitation after an accident, the insurer may assert a reimbursement claim against the settlement. Disputes usually focus on:

- Whether all billed services are accident-related

- Whether the claimed amount reflects what was actually paid

- Whether repayment should be reduced to avoid an inequitable result

How Florida vs. Texas Differences Can Affect Subrogation Leverage

State-specific rules can materially affect how subrogation is enforced:

- Texas: “Made whole” principles may limit reimbursement when the injured person was not fully compensated, depending on plan language and case facts.

- Florida: Reimbursement may be allowed but often becomes a reduction issue to prevent unfair outcomes.

These differences commonly surface in auto collision cases and early post-accident decision-making, including steps outlined in an after-car-accident checklist:

Hospital Liens and Medical Provider Claims

A medical lien is more than a bill it is a legal claim designed to attach directly to settlement proceeds.

Texas Hospital Lien Requirements

Texas hospital liens are governed by strict statutory rules. Enforceability often turns on:

- when treatment occurred

- whether statutory conditions were met

- how much of the settlement may legally be reached

Failure to comply with these requirements can limit or eliminate recovery.

Florida Hospital Lien Ordinances

Florida does not have a single statewide hospital lien statute. Instead, enforceability is often governed by county-level ordinances, which can vary in:

- filing deadlines

- notice requirements

- scope of recoverable charges

Because of these variations, lien validity frequently becomes a dispute issue.

Medicare and Medicaid Reimbursement Takes Priority

Federal reimbursement claims often operate as priority obligations that must be resolved before settlement funds can be safely distributed.

Medicare Conditional Payment Claims

Medicare may issue a conditional payment summary identifying services it believes are injury-related. These summaries often require careful review because they may include:

- unrelated treatment

- duplicate charges

- services not causally connected to the injury

Medicaid Reimbursement Reductions

Medicaid recovery may allow reductions depending on allocation, settlement structure, and case-specific factors. Negotiation often focuses on preserving a reasonable net recovery while complying with reimbursement rules.

How Lien Strategy Can Increase Your Net Settlement

Lien resolution is often the difference between a disappointing outcome and a meaningful recovery.

Reviewing Unrelated or Excessive Charges

Claims are frequently reduced by identifying:

- treatment unrelated to the injury

- unsupported billing

- documentation or coding errors

Procurement Cost and Common-Fund Reductions

When lienholders benefit from the legal work required to obtain settlement funds, proportional reductions may apply so reimbursement reflects the cost of creating the recovery.

Proportional Allocation When Liens Exceed the Settlement

When total medical claims exceed available funds, negotiations may shift toward proportional allocation so each party accepts a reduced share rather than one claim consuming the entire settlement.

Why Injury Settlement Checks Are Often Delayed

Settlement delays are most commonly caused by lien resolution not insurer inaction. Funds are typically not released until payoff amounts are finalized and reimbursement obligations are satisfied.

FAQs

Why can’t I receive my settlement immediately?

Settlement funds are usually held until lien amounts are confirmed and resolved to avoid repayment exposure.

What happens if medical bills exceed the settlement?

Proportional allocation is often negotiated so no single claim absorbs the entire recovery.

Should I use health insurance if it creates a subrogation claim?

Using health insurance often results in lower negotiated rates, which can reduce total reimbursement later.

Can ignoring Medicare reimbursement cause problems?

Yes. Failure to resolve applicable reimbursement obligations can lead to repayment demands and penalties.

Do medical liens still matter if bankruptcy is involved?

Some lien issues may persist depending on lien type and structure. Related considerations are addressed under bankruptcy.

Protect Your Settlement From Unnecessary Reductions

Medical liens and subrogation claims can quietly reduce an injury settlement if they are not carefully reviewed and negotiated. United Law Group focuses on evaluating lien validity, disputing unrelated or excessive charges, and pursuing reductions that help clients retain more of their recovery.

If your injury occurred in Florida or Texas, you can request a confidential case evaluation.