Proof of Loss Deadlines Explained: Why Late Insurance Forms Trigger Claim Denials

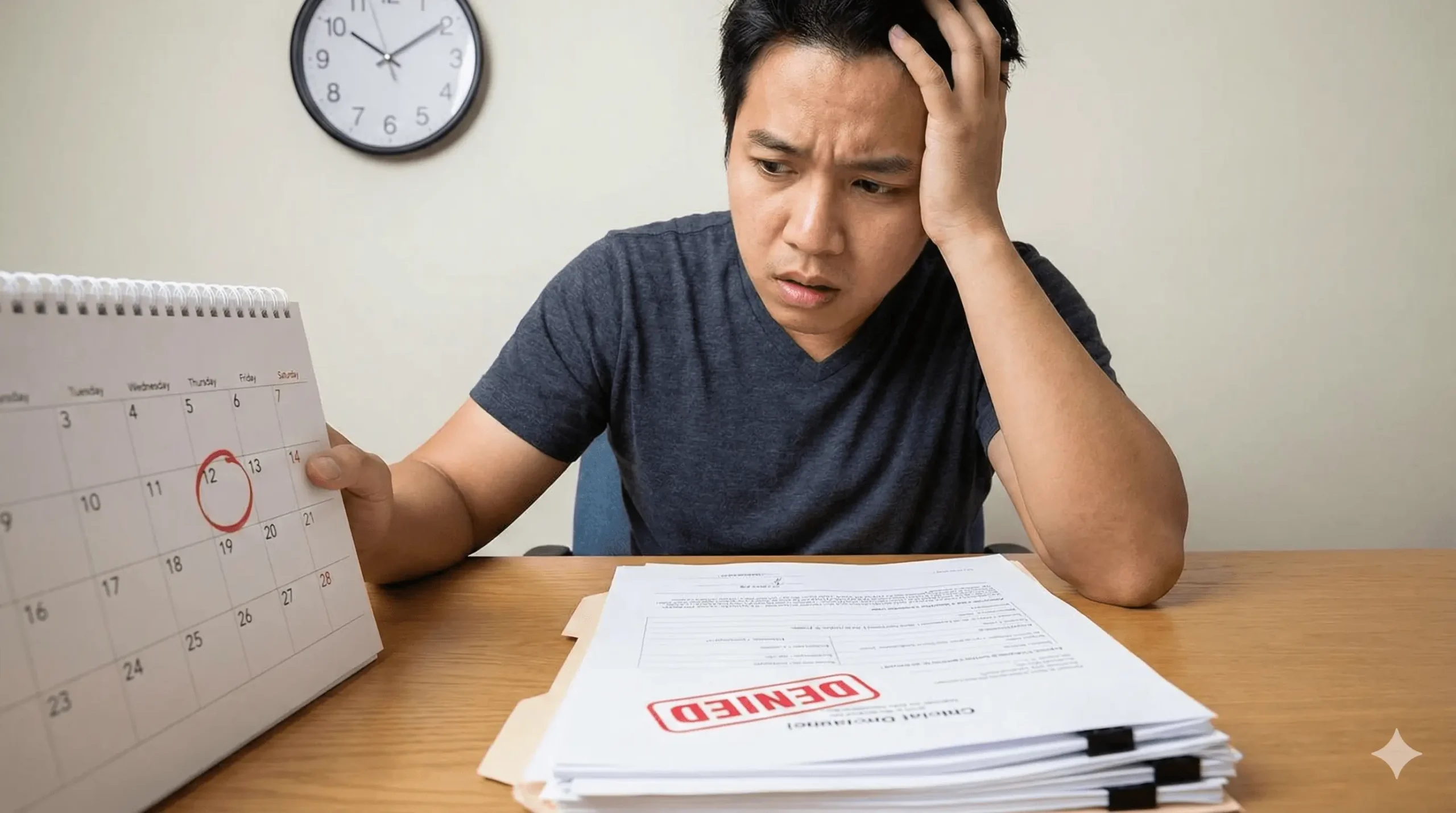

Missing a proof of loss deadline is one of the fastest ways an insurance company can deny an otherwise valid claim. These deadlines are contractual obligations, not flexible guidelines, and even short delays can eliminate your right to payment.

Proof of loss forms act as sworn statements that activate an insurer’s duty to evaluate and pay a claim. When deadlines are misunderstood or documentation is incomplete, coverage can be lost even when damage is clearly covered under the policy.

What a Proof of Loss Is and Why Insurance Companies Enforce It

A proof of loss is a formal declaration that documents what was damaged, how the loss occurred, and the amount being claimed. Once requested, it becomes a required condition that must be satisfied before payment is owed.

The Legal Purpose Behind Proof of Loss Requirements

Insurance companies rely on proof of loss forms to create a fixed, sworn record of the claim. This allows adjusters to evaluate coverage, apply exclusions, and control valuation disputes before settlement discussions begin.

In complex property disputes including large-scale losses similar to those seen in Florida condo damage claims insurers often rely heavily on proof of loss timing to limit exposure.

Because proof of loss requirements are contractual, courts frequently uphold denials based solely on late or defective submissions, regardless of damage severity.

Proof of Loss Deadlines That Apply to Your Insurance Claim

Deadlines vary based on policy language, insurance type, and state law. Misunderstanding which deadline applies is one of the most common reasons claims fail.

Homeowners Insurance Deadlines

Most homeowners policies require proof of loss submission within 60 days of the insurer’s written request, not the date of loss. Some policies instead calculate deadlines from the loss date, which can shorten the available window significantly.

This distinction becomes critical after completing the initial reporting steps involved in how to file a property damage claim, which do not replace formal proof requirements.

Commercial Property Insurance Deadlines

Commercial policies typically allow up to 90 days, reflecting the complexity of inventory valuation, equipment loss, and business interruption calculations. Extensions are common but must always be confirmed in writing before the original deadline expires.

Auto Insurance and Total Loss Deadlines

Routine auto repairs may not require formal proof of loss forms, but disputes involving total loss determinations or valuation disagreements often trigger strict documentation deadlines. These requirements can also delay recovery in personal injury cases involving vehicle damage, where coverage disputes affect settlement timelines.

Flood Insurance Proof of Loss Deadlines (NFIP)

Federal flood claims impose one of the strictest standards: proof of loss must be submitted within 60 days of the flood event, with limited exceptions. Missing this deadline can void the entire claim regardless of inspection findings or repair estimates.

What Insurance Companies Require in a Valid Proof of Loss

Submitting a form alone is rarely sufficient. Insurers expect complete documentation that supports every dollar claimed and aligns with policy conditions.

Required Forms, Valuations, and Supporting Documentation

A valid submission typically includes a fully completed and notarized form, a detailed property inventory, photographs of damage, itemized contractor estimates, and proof of ownership. High-value items often require professional appraisals.

Claims involving recurring or region-specific damage patterns including losses tied to Texas home property damage causes are often scrutinized more aggressively when documentation is incomplete.

Why Incomplete Proof of Loss Submissions Are Rejected

If required materials are missing, insurers may treat the submission as never having been made. This technical distinction allows carriers to deny claims once the deadline passes, even if partial documentation was provided earlier.

Why Insurance Claims Are Denied for Missed Proof of Loss Deadlines

Proof of loss deadlines are treated as conditions precedent obligations that must be satisfied before coverage applies.

Common Reasons Policyholders Miss Proof of Loss Deadlines

Deadlines are frequently missed while waiting on contractor estimates, misunderstanding when the clock starts, or assuming adjusters handle submissions. Communication breakdowns following disasters or serious accidents further increase risk.

In some cases, deadline denials may intersect with broader issues governed by consumer protection laws, particularly when insurers fail to provide proper notice or guidance.

Financial Consequences of Deadline-Based Claim Denials

Once denied, claims are difficult to revive. Lost recoveries may include repair costs, temporary housing expenses, or business income losses that often far exceed the effort required to meet submission deadlines.

How to Request a Proof of Loss Deadline Extension the Right Way

Extensions are possible, but only when requested properly and before the original deadline expires.

What Insurers Consider When Reviewing Extension Requests

Insurers typically evaluate claim complexity, third-party delays, disaster-related backlogs, and documented hardship. Requests must be specific, supported, and confirmed in writing. Submitting partial documentation before the deadline strengthens good-faith arguments if disputes arise later.

What Options Exist After Missing a Proof of Loss Deadline

Missing a deadline does not always eliminate recovery, but success depends on swift action and legal positioning.

Legal Arguments That May Preserve a Late Insurance Claim

Arguments such as waiver, estoppel, substantial compliance, or lack of insurer prejudice may apply when carriers continue negotiations or fail to provide proper notice. These issues often surface alongside broader disputes involving property damage handling standards.

State-specific claim rules can also affect outcomes in Florida and Texas property damage matters.

FAQs

Can insurers deny claims even when damage is clearly covered?

Coverage alone does not override contractual obligations. Proof of loss deadlines operate independently from coverage determinations, allowing insurers to deny payment even when damage is undisputed.

Does late documentation invalidate an otherwise complete claim?

Supplemental documentation is usually allowed when the original submission is complete and timely. Problems arise when required valuation data is missing at the deadline.

Are proof of loss deadlines enforced differently after major disasters?

Regulatory extensions may apply after catastrophic events, but they are not automatic. Policyholders must confirm whether official deadline relief applies to their specific claim.

How to Protect Your Insurance Claim From Deadline-Based Denials

Proof of loss deadlines are among the most unforgiving aspects of insurance claims. Understanding how they work and how insurers enforce them is critical to protecting recovery.

United Law Group assists policyholders in challenging deadline-based denials, evaluating insurer conduct, and pursuing recovery across property damage, personal injury, and consumer protection matters. When insurers rely on missed paperwork to avoid payment, a timely legal review can determine whether enforceable options still exist.