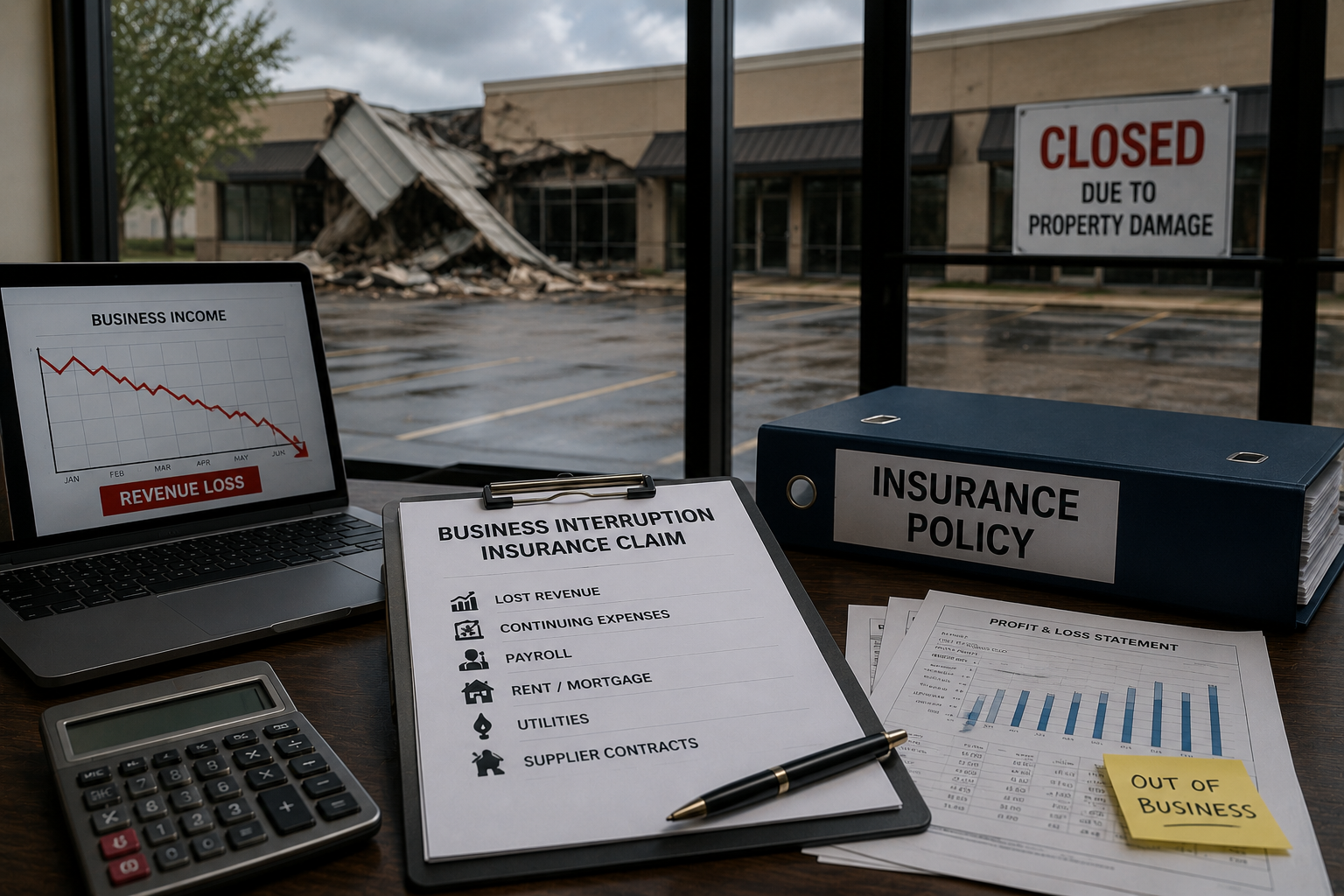

Texas Business Interruption Insurance Claims

If you are searching for a business interruption insurance claim lawyer Texas owners rely on, your business probably shut down after a storm or fire and the carrier is dragging its feet on the lost income. That income is often the largest part of the claim, and the part insurers fight hardest.

This guide explains what business interruption coverage pays, how carriers undercount it, and how Texas law helps you push back. For the bigger picture, see our Texas commercial property damage page.

What Business Interruption Coverage Actually Pays

Business interruption coverage, sometimes called business income coverage, exists to put your business where it would have been financially if the loss had never happened. It is built into most commercial property policies, though many owners do not realize they have it until disaster strikes.

In plain terms, it generally pays your lost net income plus the continuing expenses you still owe while you cannot operate, like rent, loan payments, and payroll you choose to keep. The coverage runs through the period of restoration, the time it reasonably takes to repair the property and reopen.

The key word is net income. The claim is built on the profit you would have earned, not your gross sales, so it accounts for the costs you saved by being closed as well as the expenses that continued. Getting that calculation right, and documenting both sides of it, is what separates a full payout from a lowball one.

Many owners are surprised to learn how broad the coverage can be. Beyond the obvious lost sales, it can reach commissions, contracts you could not fulfill, and the slow ramp-up after reopening. The coverage is there to make the business whole, and a complete claim looks at the full arc of the disruption, well beyond only the days the doors were physically locked.

Many policies add extra-expense coverage on top, which pays the costs of getting back up and running faster, such as renting a temporary location, leasing equipment, or paying overtime. Used well, extra-expense coverage can shorten the shutdown and reduce the overall loss.

There is usually a waiting period, often 48 to 72 hours, before coverage kicks in, and a coverage cap or time limit on the far end. Knowing those limits up front matters, because they shape how the claim is built and how quickly you need to act. We read your specific policy rather than rely on what a typical policy says.

Business interruption sits alongside the building claim, not in place of it. The physical-damage claim pays to repair the property, and the business-interruption claim pays for the income lost while that repair happens. Our Texas commercial property damage page covers the property side, and the two claims are usually pursued together.

Closed after a covered loss? Call (727) 306-3324 or request a free case evaluation.

Triggering Events: Fire, Storm, and Shutdown

Business interruption coverage usually requires a direct physical loss to your property from a covered peril. The most common triggers in Texas are fire, hail, windstorm, and hurricane damage that forces you to close or scale back operations.

The link between the physical damage and the lost income is where disputes start. If a fire guts your kitchen, the lost restaurant revenue clearly flows from a covered loss. If a storm damages a neighbor’s building and the city closes the block, coverage gets murkier, and that is where the policy language matters.

Pandemic-era litigation sharpened these fights, with courts across the country parsing what counts as direct physical loss. The practical takeaway for Texas businesses is that the exact policy wording, and the cause of your shutdown, drive whether coverage applies, so a careful read of your specific policy against your specific facts is essential before you accept a denial.

Civil-authority and ingress-egress provisions can extend coverage when a government order or blocked access shuts you down even without direct damage to your own building. These clauses are narrow and heavily litigated, so reading them carefully against your facts is essential.

Texas businesses see these triggers most often after hurricanes and severe storms, when a single weather event damages a property, knocks out power, and closes roads all at once. Sorting out which losses flow from your covered physical damage and which flow from an excluded cause is a big part of the fight, and the policy wording controls the answer.

Timing of the trigger also matters. Coverage generally starts at the date of the physical loss and runs through the restoration period, so pinning down exactly when the damage occurred and when you could reasonably have reopened frames the entire claim. We document both ends of that window carefully.

Restaurants, retailers, and service businesses each feel these triggers differently. A restaurant loses perishable inventory and every dining-room shift the moment the power goes, a retailer loses foot traffic and online fulfillment, and a clinic loses billable appointments. We match the claim to how your specific business earns, because a generic template misses losses unique to your operation.

How Insurers Undercount Lost Income and the Restoration Period

Business interruption is the easiest part of a claim for an insurer to shrink, because it rests on projections rather than a stack of repair invoices. The carrier has every incentive to assume your business would have earned less and recovered faster than it really would.

The restoration period is where they cut most. They assume repairs that drag on for months could have been done in weeks, then pay only for that shorter window. We document why the realistic timeline is what it is, including permitting, contractor availability, and supply delays.

They also dispute your projected revenue, ignore seasonal swings, and leave out continuing expenses you genuinely carried. Each assumption quietly lowers the payout, and because the math is complex, owners often do not notice how much was shaved off.

A common trick is to value your lost income off a slow stretch rather than your real trend. A restaurant hit right before its busy season, or a retailer closed through the holidays, loses far more than a flat monthly average suggests. We build the projection off your actual history so the seasonal reality is baked in.

Another is to treat your payroll as a cost you should have simply cut. Many owners keep paying key staff to avoid losing them, and that continuing payroll is often recoverable. Letting the insurer assume you laid everyone off undercounts both your expenses and your ability to reopen quickly.

They also lean on the duty to mitigate, arguing you could have reopened sooner or limited the loss, then using that to shave the claim. Mitigation is a real obligation, but it does not mean accepting an unrealistic timeline the adjuster invents. We document the steps you actually took and why the restoration took as long as it did.

Think your lost-income payout fell short? Call (727) 306-3324 or request a free case evaluation.

Proving Your Losses: The Financials the Adjuster Wants

Business interruption claims are won with documents. The stronger your financial record, the harder it is for the carrier to lowball you. The core proof usually includes:

- Profit-and-loss statements from before the loss

- Tax returns for the prior years

- Monthly sales records showing trends and seasonality

- Payroll and fixed-expense records

- Any projections or contracts showing expected future revenue

We often work with forensic accountants to build a defensible projection of what your business would have earned, then measure the gap against what it actually did. That analysis turns a squishy lost-income claim into a number the carrier has to take seriously.

Newer businesses face an extra hurdle, because they have less history to project from. It is still doable with industry data, comparable locations, booked contracts, and the trend you had before the loss, but it takes more care. We do not let a short track record become the insurer’s excuse to pay almost nothing.

The goal is to show the income the interruption truly cost you, including the ramp-up period after you reopen, when revenue often lags while customers return. Insurers like to cut the claim off at the reopening date, but the loss frequently continues past it.

Cooperate with reasonable document requests, but be careful about how the information is framed. Adjusters sometimes ask questions designed to lock you into a low revenue estimate or an early reopening date. Having the numbers organized and presented correctly from the start keeps the claim anchored to reality rather than to the insurer’s assumptions.

Chapter 542A and Prompt-Payment Pressure

Texas law gives business-interruption claimants real footing. When the loss stems from a force of nature like a storm or hurricane, Texas Insurance Code Chapter 542A applies, with its 61-day pre-suit notice that spells out what the insurer owes.

The Prompt Payment of Claims Act in Texas Insurance Code Chapter 542 adds interest, historically up to 18 percent per year, plus attorney fees when the insurer misses claim-handling deadlines. For a business bleeding income during a shutdown, that penalty is a powerful reason for the carrier to pay promptly.

When an insurer denies a valid business-interruption claim or delays without a reasonable basis, Texas Insurance Code Chapter 541 and the common-law duty of good faith can expose it to damages beyond the policy. We use these tools together to move a stalled claim.

These remedies matter even more for business interruption than for a building claim, because the harm compounds daily. Every week the insurer delays is another week of lost revenue you cannot get back, and the prompt-payment interest and bad-faith exposure give the carrier a financial reason to stop stalling and pay what it owes.

What to Do When a BI Claim Is Denied

A denial or a lowball offer is the start of a negotiation, not the end. The first step is understanding exactly why the carrier said no, because the reason points to the fix.

- Keep operating records and document every day you are closed or limited

- Preserve the financials that prove your pre-loss income

- Track every extra expense you incur to reopen

- Do not accept a quick payout before the full loss period is known

- Get the policy reviewed for civil-authority and extra-expense coverage

Act before the deadlines close in. Weather claims require the 61-day pre-suit notice, and the suit deadline is generally two years, so a stalled claim can quietly run out of time while you wait on the carrier. The sooner the claim is built and the notice is sent, the more options you keep.

Most owners undervalue these claims because the math is hard and the carrier sounds confident. A review often reveals coverage and losses the insurer ignored, from extra-expense provisions to a longer restoration period than the adjuster allowed. Our bad-faith and underpayment tactics guide shows the moves to watch for.

How We Help

We read the policy for every applicable coverage, build the lost-income proof with forensic accountants, send the Chapter 542A notice, and pursue the prompt-payment and bad-faith remedies when the carrier will not pay fairly. We handle the dispute so you can focus on reopening. Our Texas property damage page covers the full range of these claims.

We work on contingency, so there is no upfront cost and no hourly bill. We only get paid if we recover for you, and the consultation is free. For a business already losing money, that arrangement means challenging an unfair denial costs you nothing out of pocket.

We also move on the timeline these claims demand. Lost income compounds every week, so we build the financial proof, send the Chapter 542A notice, and press the prompt-payment clock without waiting for the carrier to come around on its own. The faster a stalled claim gets moving, the less revenue slips away for good.

Talk to a Texas Business Interruption Lawyer

If your business-interruption claim was denied or underpaid, a free review will tell you whether it is worth fighting and what it is realistically worth. Owner Jack Vasilaros reviews these claims personally.

We work on contingency, so you pay no fee unless we win, and the consultation is always free with no obligation. Jack’s got your back from the first call to the final check, and we keep you updated at every step.

What does business interruption insurance cover in Texas?

It generally pays your lost net income plus continuing expenses, like rent and payroll, during the period of restoration after a covered physical loss. Many policies also add extra-expense coverage to help you reopen sooner.

What triggers business interruption coverage?

Usually a direct physical loss to your property from a covered peril such as fire, hail, windstorm, or hurricane that forces you to close or scale back. Civil-authority and ingress-egress clauses can extend coverage to some government-ordered closures.

How do insurers undercount these claims?

They shorten the restoration period, dispute your projected revenue, ignore seasonality, and leave out continuing expenses. Because the claim rests on projections, those cuts are easy to hide without strong financial proof.

How do I prove my lost income?

With profit-and-loss statements, tax returns, monthly sales records, and payroll and expense documents, often supported by a forensic accountant who projects what the business would have earned.

Does Texas law help with a delayed claim?

Yes. The Prompt Payment Act adds interest and attorney fees when an insurer misses deadlines, and Chapter 542A and the bad-faith laws add pressure when a valid claim is denied or delayed.

How long do I have to act in Texas?

Generally two years from the denial or underpayment, and weather claims require a 61-day pre-suit notice before filing, so it is best to start early.

What does it cost to hire a lawyer?

Nothing upfront. We work on contingency, so you pay no fee unless we win, and the consultation is free.